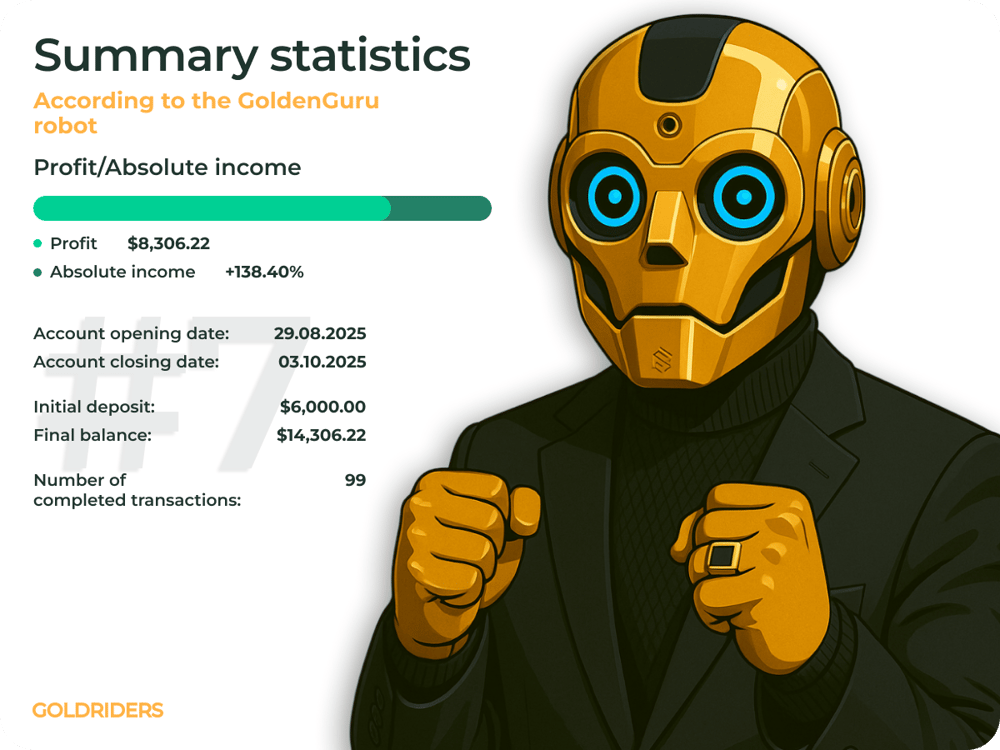

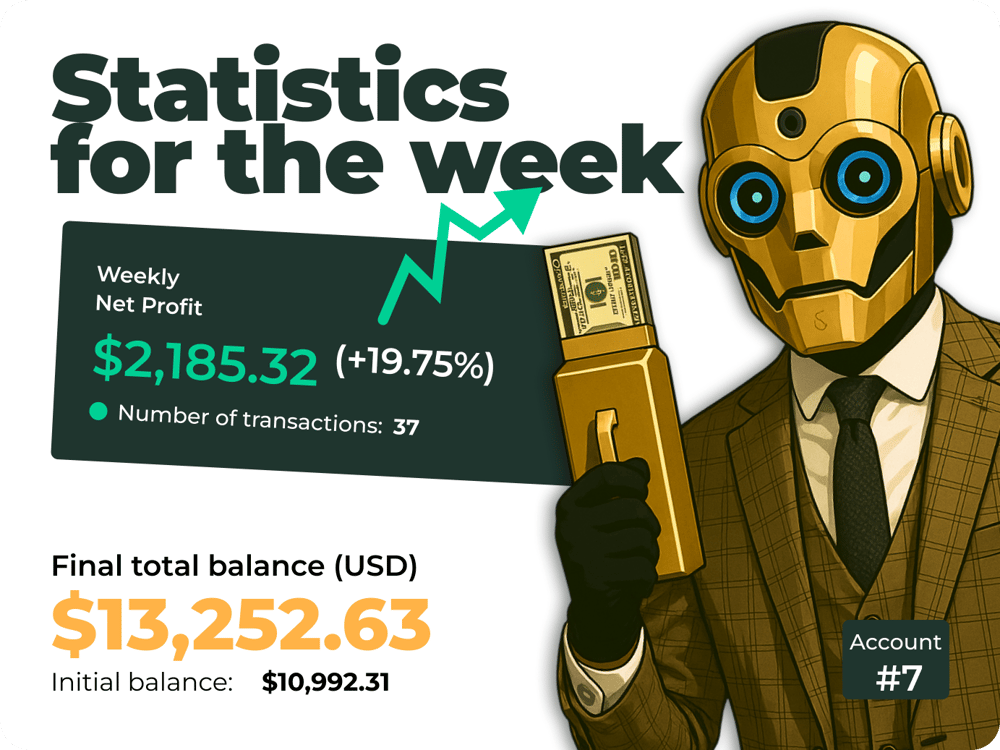

Another week is behind us and once again, with results. The GoldenAI automated trading system continues to deliver stable performance in a dynamic market. Every trade has been carefully analyzed, and the latest report is now ready.

Another week is behind us and once again, with results. The GoldenAI automated trading system continues to deliver stable performance in a dynamic market. Every trade has been carefully analyzed, and the latest report is now ready..

More and more traders are switching to automated trading on Forex and cryptocurrency markets. Trading advisors (robots, Expert Advisors, bots) help save time, reduce emotional pressure, and stabilize results. But one of the most common questions is: do you need to update a trading robot, or can it work “forever”?

The current hype of memcoins has gained terrible momentum, the crypto space is filled with conversations only about this. In today's article, we'll look at what memcoins are, who makes money from them and how, why they should be listed on exchanges, and most importantly, what we should do with you.

In recent years, trading robots (algorithmic trading systems) have become increasingly prevalent tools across various markets, including forex pairs like USD and EUR, as well as equities such as Apple Inc. (AAPL) $AAPL and major indices like the S&P 500 (SPX) $^GSPC. Automation enables faster execution and reduces emotional bias in trading decisions. However, a critical question arises: how safe and effective is it to entrust your investments to a trading robot?

Financial markets today are witnessing a surge in the use of algorithmic trading systems to automate trades. Currency pairs such as USD/EUR $USDEUR, stocks like Apple Inc. $AAPL (AAPL), and the S&P 500 Index (SPX) $^SPX rank among the most liquid and widely traded assets, where trading robots play a key role in enhancing trade speed and accuracy. Amid volatile markets and high information flow, these automated systems assist traders and institutional investors in minimizing human errors and swiftly reacting to market shifts.

Ambarella Inc. $AMBA shares surged over 17% during Tuesday’s morning session following reports that the California-based semiconductor firm is exploring strategic alternatives, including a possible sale. The spike in share price reflects mounting investor optimism regarding a potential acquisition at a premium valuation. Headquartered in Santa Clara, Ambarella specializes in edge AI processors, particularly for automotive and computer vision applications. With a current market capitalization of approximately $2.3 billion, the company has reportedly engaged investment bankers and approached multiple potential buyers, according to sources familiar with the matter.