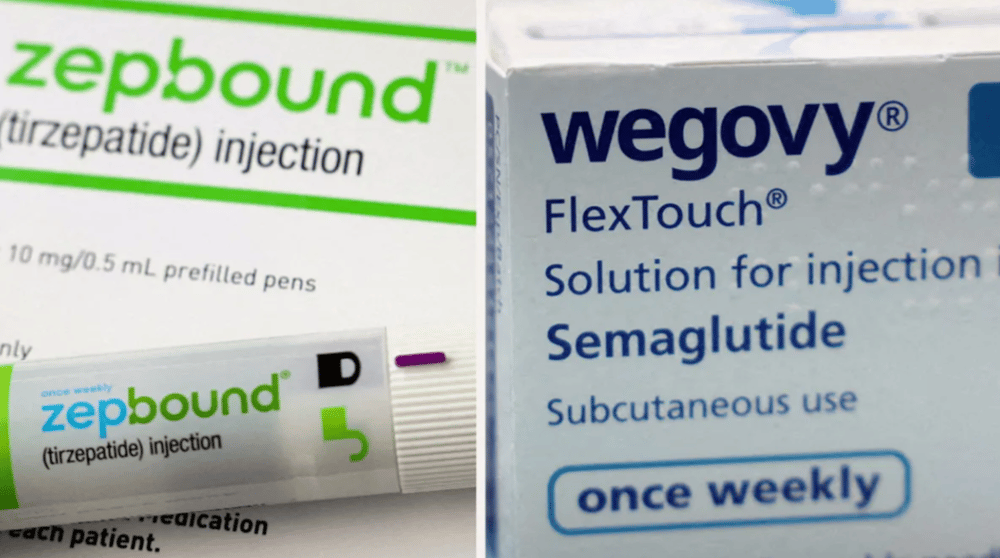

Eli Lilly $LLY has intensified its presence in the surging obesity drug market with new clinical data that places its medication, Zepbound, ahead of Novo Nordisk’s $NOVO-B.CO Wegovy in five key metrics of weight reduction. Released on Sunday, the results of the first head-to-head study between the two blockbuster drugs underscore Lilly's competitive advantage just as the sector is projected to exceed $150 billion annually within the next decade.

The comparative trial, revealed at the European Congress on Obesity, adds clinical heft to Lilly’s claims made in December — that patients using Zepbound experienced 47% greater weight loss than those treated with Wegovy. These findings come at a time when insurance coverage and drug formulary access are playing an increasingly pivotal role in defining the commercial viability of these treatments.

Zepbound’s Clinical Highlights Redefine the Standards

The results arrive in the wake of growing insurer scrutiny, including a recent decision by CVS Health $CVS to remove Zepbound from certain covered drug lists in favor of Wegovy. However, the latest data may give Lilly new leverage in payer negotiations and formulary battles, particularly as real-world efficacy becomes a defining factor in drug adoption.

Greater total weight loss: Zepbound consistently led to higher average weight reduction over the study period.

Reduced waist circumference: Patients on Zepbound saw more significant reductions in abdominal fat — a key cardiovascular risk marker.

Lower BMI readings: Across diverse demographic groups, Zepbound showed stronger results in decreasing body mass index.

Improved metabolic indicators: The drug was associated with better control of blood sugar and insulin sensitivity.

Patient-reported outcomes: Participants reported enhanced quality of life and greater satisfaction compared to Wegovy.

Strategic Implications for Market Leaders

Reinforced Clinical Positioning Eli Lilly now holds robust comparative data, strengthening Zepbound's profile in the highly competitive obesity market.

Negotiating Power with Insurers Despite recent formulary setbacks, Lilly may use this evidence to re-engage payers such as CVS Health, emphasizing long-term cost savings through superior efficacy.

Shifting Consumer Demand Patients and healthcare providers may increasingly opt for Zepbound based on measurable improvements in outcomes and overall health metrics.

Regulatory and Global Expansion Opportunities With comparative effectiveness now demonstrated, Lilly is better positioned for regulatory wins and broader global market penetration.

Valuation Support for Eli Lilly Investors tracking Eli Lilly may view these developments as reinforcing long-term growth trajectories in its obesity and diabetes portfolio, particularly as demand outpaces supply across global markets.

Navigating a Rapidly Evolving Therapeutics Landscape

The obesity drug sector is evolving into one of the most lucrative and scientifically dynamic areas in pharmaceutical development. The showdown between Zepbound and Wegovy represents a broader trend toward clinical superiority dictating market leadership. Eli Lilly’s ability to outmaneuver formulary exclusions with hard data may signal a shift in how reimbursement decisions are made in the high-stakes world of weight-loss therapeutics.

Still, commercial execution will be critical. While clinical results favor Zepbound, market dominance hinges on accessibility, pricing strategy, and sustained manufacturing capacity. With insurers like CVS Health reassessing cost structures, the coming months will be pivotal in determining whether Lilly can convert clinical wins into expanded market share.

This development signals growing confidence in the automation industry's long-term potential